by

by Vahit Ozalp

Introduction

Illumina (NASDAQ: ILMN) focuses on the development and production of life science tools to analyze genetic variation and function. Operating through the Core Illumina and GRAIL divisions, the company provides sequencing equipment, consumables, and whole genome and targeted sequencing kits. It offers services like genotyping, whole genome sequencing, and early detection tests for Galleri cancer. Serving research centers, academic institutions, and healthcare facilities around the world, Illumina was founded in 1998.

Recent Developments: Illumina reported Q2 earnings of $0.32, beating estimates, and revenue of $1.18B. NovaSeq X shipments increase. However, they have lowered their annual revenue and earnings guidance.

The following article discusses Illumina’s recent financial performance, legal challenges surrounding the acquisition of GRIL, and updated annual guidance. I recommend selling their stock.

Q2 earnings report

Looking at Illumina’s latest earnings report, Q2 2023 revenue stood at $1.176B, a slight increase from Q2 2022’s $1.162B. The gross margin is reduced to 62.2% from 66.0%. R&D expenses increased to $358 million from last year’s $327M. SG&A expenses also saw an increase from $410M to $450M. A significant decrease was noted in the case of legislation and settlements, from $ 609M in Q2 2022 to only $ 12M in Q2 2023. The operating profit showed an improvement, reaching $ 82M in Q2 2023 from a loss of $ 579M in Q2 2022.

Cash Flow and Writing

Turning to Illumina’s balance sheet, as of July 2, 2023, the company had a combined total of $1.6B in ‘cash and cash equivalents’, ‘short-term investments’, and ‘investments’. For the six months leading up to this date, the company reported net income from operations of $115M, or about $19.2 million per month. With monthly cash flow, it shows that the company adds about 19.2 million dollars to its resources every month. Looking at consolidated assets and positive cash flow for the month, it is imperative to mention that these figures are based on historical data and may not be a direct indication of future performance.

As for solvency, Illumina’s current assets exceed current liabilities by nearly $1B, even after accounting for the EU fine. This suggests a strong short-term financial position. The company has senior convertible notes valued at $750M and term notes amounting to $1.5B, reflecting its long-term commitments. While Illumina has significant debt, its cash flow from operations and significant cash reserves could enable it to turn to additional financing, if needed. However, these details are mine, and other reviewers may have a different interpretation of the information.

Assessment, Growth, and Treatment

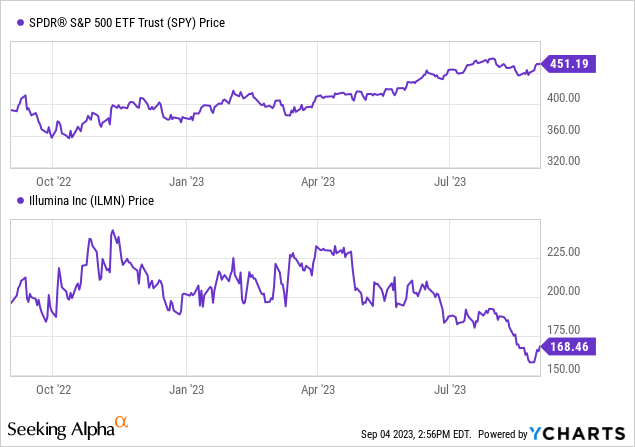

According to data search Alpha, Illumina’s capital structure shows an average level of debt compared to its market capitalization, with an enterprise value of $28.16B. Its classification of the metrics of importance of the signal passed is given forward P/E and EV multiples. The company is generating little revenue growth. Illumina’s stock performance is weak, underperforming the S&P500.

Recent developments, including strong Q2 earnings and the shipment of the NovaSeq X, are commendable. However, lower guidance for the year and legal challenges surrounding GRIL’s acquisition pose potential concerns. This is coupled with a downward spiral in future earnings growth and significant revisions to operational and market challenges. While the long-term outlook for the genomics sector remains promising, Illumina is facing headwinds that require a strategic move.

Illumina’s GRAIL: Divine Discovery or Evil Control?

Based on Illumina’s latest 10-Q SEC filing (Under “7. Legal Procedures”)Here is a summary of the legal implications surrounding their acquisition of GRIL:

Both the US and the EU have scrutinized Illumina’s acquisition of GRIL. In the US, the Federal Trade Commission [FTC] he believed the deal could “harm” competition. Although the FTC initially lost its case, it later asked Illumina to drop GRIL, a decision that Illumina is challenging. In the EU, the European Commission found that the acquisition could restrict competition. As a result, on July 12, 2023, they fined Illumina approximately 432 million euros (equivalent to 471 million dollars received by the company) for violating the EU Merger Regulation. Illumina plans to appeal the ruling. Furthermore, in July 2023, the SEC notified Illumina of an investigation into GRIL’s acquisition in the US, focusing on GRIL’s disclosures among other concerns. Illumina is committed to assisting with this research.

My opinion: Because the SEC’s probe is focused on the revelations of Illumina about GRIL and the actions of certain management figures, it seems possible that they are investigating violations of federal securities laws. These laws ensure the transparency, fairness, and equity of contracts. Should the SEC determine that there were misleading statements or omissions that misled investors or regulatory bodies, Illumina could face significant fines. The amount of fines that can be imposed by the SEC can vary, potentially from thousands to millions, based on the severity and consequences of the alleged misconduct. In addition, it is important to understand that an SEC investigation can lead to wide-ranging implications, affecting the company’s image, investor confidence, and stock valuation.

Illumina’s Genomic Jitters: Sequencing Challenges

Illumina’s recent decision to cut its full-year compounded revenue growth guidance from an initial range of 7% to 10% to around 1% highlights some of the headwinds the company may face in its operating environment. Due to the San Diego-based firm’s position in the genomic sequencing market, such significant cuts reflect external market conditions, competition, or internal challenges that may affect its financial performance.

In the rapidly evolving world of genomics and genetics research, companies like Illumina must continue to innovate to stay competitive. Reduced revenue guidance could reflect increased competition or potential challenges in meeting high expectations in the sector. In addition, there are changes in consumer preferences or disruptions in the supply chain, which may lead to reduced sales or increased operating costs.

A downward revision of adjusted earnings per share from a range of $1.25 to $1.50 to a lower bracket of $0.75 to $0.95 further underscores the financial pressure. These significant reductions may be a reflection of higher operating costs, reduced margins due to price pressures, or unexpected costs, which may be caused by regulatory or legal challenges, such as the aforementioned sourcing concerns.

In the broader context of the genomic market, advances in human medicine and ongoing research in genomics remain strong. Thus, while Illumina may face short-term challenges, the long-term outlook for companies in the genomic space remains promising, due to the increased reliance on genetic data in the health, research, and consumer sectors. However, Illumina’s updated guidance serves as a reminder of the complexity and rapid changes that exist in this market.

My Analysis and Recommendation

Illumina presents a mix of recent advances and upcoming challenges. While their Q2 2023 earnings showed recovery, the legal headwinds associated with the GRIL acquisition pose potential financial and reputational risks. Most notable is Illumina’s decision to significantly reduce its annual revenue and earnings guidance, likely influenced by heightened competition, supply chain disruptions, or unexpected administrative costs.

In the coming weeks, the results of the legal challenges will be important. They have the potential to significantly impact Illumina’s financial health and market position. Additionally, Illumina’s ways of working through these turbulent times will provide insight into their flexibility and prospects in the emerging genomics sector.

Considering the uncertainty surrounding the GRAIL acquisition and revised financial guidance, I recommend a “Sell” position on Illumina. The current landscape suggests potential volatility in the short to medium term, making it prudent for investors to reconsider their position. However, individual financial goals and risk tolerance should always guide investment decisions.

Risks in Thesis

While my analysis on Illumina is based on the latest financial data and business developments, there are several potential risks and considerations that may weigh against my final investment recommendation:

-

10 Best Ignored Indicators: While there are significant challenges, I wouldn’t overlook certain growth drivers or long-term strategic moves that could increase Illumina’s value in the future.

-

External Issues: Outside opinions, especially negative ones, may have influenced my evaluation more than they should have.

-

Overestimation of Legal Risks: The legal battles may be protracted and uncertain, but the end results may be far more dangerous than currently anticipated.

-

Underestimation of Sector Skills: The genomic sector is ripe for exponential growth. If Illumina navigates its current challenges successfully, it could be well-positioned to benefit from broader sector growth.

-

Misconceptions about the Competitive Landscape: While I view the reduced guidance as a possible sign of heightened competition, it is likely that the reasons are temporary and will not significantly impact long-term pricing.

-

Recovery Guidelines: Q2 2023 showed a recovery, which may indicate a trend rather than an anomaly.

-

Side guarantee: My decisions may lean heavily on data that supports a “Sell” recommendation, which may be overridden by contrary information.

#Illumina #Genetic #Plot #Twist #Time #Reveal #Stock #NASDAQILMN